Constellation Stock #3: DraftKings Inc. (DKNG) - Growth Story

As the map of legal online gambling continues to broaden, DraftKings' early and aggressive expansion efforts are paying off, marking it as a key player in the market.

Intro

Sports betting is legal in 37 states and Washington D.C., with other states drafting legislation, leaving 12 more (and some additional territories) left to tap. This expanding legality opens significant market opportunities for industry leaders.

As more states open their doors to the gambling business, DraftKings stands at the forefront of this booming industry, leveraging the tailwind of increased legalization to fuel its ascent. The company's agile adaptation to new markets and its ability to attract and retain a growing base of users underscores its potential for sustained growth.

Company Overview

DraftKings Inc. operates as a digital sports entertainment and gaming company in the United States and internationally. It provides online sports betting and casino, daily fantasy sports, media, and other consumer products, as well as retail sportsbooks. The company also engages in the design and development of sports betting and casino gaming software for online and retail sportsbooks, and iGaming operators. In addition, it offers DraftKings marketplace, a digital collectibles ecosystem designed for mainstream accessibility that offers curated NFT drops and supports secondary-market transactions. Although its roots are in the fantasy sports business, 2018's end to the United States federal ban on sports wagering has proven a boon for the company.

Last Close Price: $41.81

Shares out: 473.62M

MCap: ~ $19.77 B

Next Earnings Date: May 2, 2024

Short Interest: 4.16%

Sector: Consumer Discretionary

Industry: Gambling

Revenue Streams

Daily fantasy sports contests: enthusiasts pay entry fees to compete based on their sports knowledge and analytical skills. This platform allows users to engage in a variety of sports, leveraging their expertise to win prizes.

iGaming: an extensive suite of online casino games, including slots, blackjack, and roulette, among others. This diversification into iGaming allows DraftKings to capitalize on the growing online casino market, generating revenue through user wagers and in-app purchases. The platform offers approximately 400 games.

Advertising: providing a space for brands to connect with a dedicated audience of sports and gaming enthusiasts, DraftKings enhances its revenue through display ads, sponsored content, and branded promotions.

Business-to-business (B2B) segment: offering its technology and software to other companies.

Recent Company News

Mar-7 2024: DraftKings Sportsbook will expand to 27 US states with the addition of North Carolina, according to the company.

Feb-12 2024: DraftKings has signed a multiyear sports betting partnership with digital media company Barstool Sports.

Jan-10 2024: DraftKings announced plans to launch its online sportsbook in Vermont. Vermont is the 26th state where its DraftKings Sportsbook operates.

Market Potential

According to Statista, The Online Gambling market worldwide is projected to reach a revenue of $107.30bn by 2024. This is expected to result in a market volume of $138.10bn by 2028, with an annual growth rate (CAGR 2024-2028) of 6.51%.

Source: Statista

QUANTS

Financial Outlook

Strong growth path:

> The Online Sports Betting (OSB) segment experienced a rise in both the total number of bets placed and Gross Gaming Revenue (GGR), with the GGR leaping from 28% to an impressive 40%.

> The Net Gaming Revenue (NGR) for OSB, which accounts for the cost of payouts, saw growth from 30% to 36%, highlighting the segment's burgeoning profitability.

> In the iGaming sector, DraftKings still reported a positive increase in GGR from 25% to 28%, reinforcing its upward trajectory in this space.4Q EPS (Non-GAAP) at 0.29 +60% vs cons at 0.18. Revenue is slightly below consensus.

Guidance raise:

> Raises FY 2024 Revenue Guidance to Range of $4.65-$4.90 Billion, Up From $4.5-$4.8 Billion, (pre-result consensus was at $4.67bn, current consensus at $4.79).

> FY 2024 Adjusted EBITDA Guidance to $410-$510 Million, vs Prior View of $350-$450 Million (pre-result consensus was at $423mn, current consensus at $473mn).KPIs: Q4 monthly unique players (MUPs) grew 37% Y/Y (75% vs 4Q21) to 3.5M (cons at 3.3m) while average revenue per MUP (ARPMUP) grew 6% YoY (50% vs 4Q21) to $116 (cons at $123) due to improvement in the company's sportsbook hold rate, partially offset by customer-friendly sports outcomes (“worst stretch of sport outcomes we have seen as a public company in the fourth quarter”).

Acquisition of lottery app company Jackpocket:

> The company is acquiring Jackpocket for around $750 million (9.6x EV/FY23 Revenues; 5.5x EV/FY24E rev), with 55% of the deal being paid for with cash on the balance sheet and 45% being paid for with common stock.

> Jackpocket is a provider of digital lottery services in the U.S. DraftKings said the deal will help the company expand in the "massive U.S. lottery industry" (new vertical, differentiating further DKNG’s product portfolio) and have higher lifetime value for its existing customers.

>Roughly 53% of Americans purchased a lottery ticket in 2021, and the total addressable market in the U.S., by some estimates, is about $100 billion.Jackpocket’s customer acquisition costs in 2023 were also 80% lower than those seen by DraftKings, the company said. As another data point, DraftKings said it looked into the tendencies of its existing customers that already overlap with Jackpocket, and concluded that those customers are worth 50% (higher spend) more over a lifetime of gaming than the customers that hadn’t engaged with Jackpocket. Put another way, Jackpocket can attract more valuable customers, and at a cheaper price, DraftKings said.

Source: DraftKings Inc. Investor Presentation

Q42023 Earnings Key Management Comments

“We expect to generate between $310 million and $410 million in free cash flow in 2024 based on approximately $120 million of annual CapEx and capitalized software development costs as well as a modest source of cash from changes in net working capital and interest income. Therefore, we will end the year with approximately $1.6 billion of cash before using approximately $413 million to fund our proposed acquisition of Jackpocket.”

“Revenue increased 64% year-over-year in fiscal year 2023... More importantly, we improved adjusted EBITDA in fiscal year 2023 by nearly $600 million year-over-year and posted our first 2 adjusted EBITDA positive quarters in company history.”

Tailwinds

Expansion. Sports betting is legal in 37 states and Washington D.C., with other states drafting legislation, leaving 12 more (and some additional territories) left to tap. DraftKings is now live in 24 states that represent around 46% of the U.S. population. The company also has iGaming live in 5 states.

As of the third quarter, the company reports it controls 33% of the United States online sports betting and iGaming market, up from 25% a year earlier. 4Q 2023 results showed that 87% customer retention over 5 years on average, improving y/y.

Progress towards profitability. 4Q23 positive EPS (second time in the company’s history, after 2Q23) permanent swing to profitability is predicted for 2024.

Active M&A policy.

Headwinds

Intense competition in the online sports betting and iGaming industry. DraftKings must innovate and differentiate to maintain its competitive edge.

November launch of Disney’s ESPN Bet platform could break the “Draftkings-FanDuel” Duopoly in sports betting. They target a 20% market share by 2027.

Regulatory complications.

Industry Comps Analysis

Source: Stockpickingsouk

DKNG is difficult to compare with its peers acting in the same segment, as it has way stronger growth prospects, but also reflected in a way higher valuation. This is due to its market share position (way larger vs peers), leading technology, and first-mover advantage.

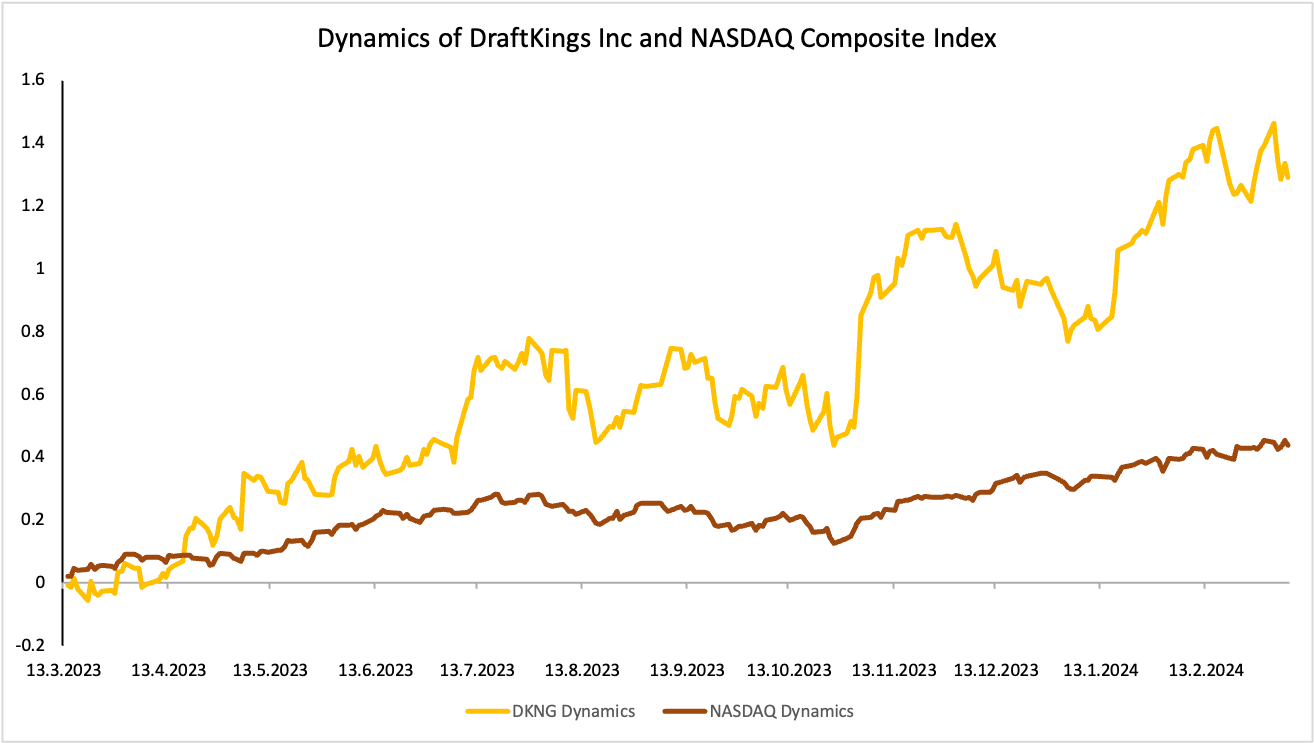

Price Action and Benchmarking

Source: Yahoo Finance

DraftKings Inc. has demonstrated higher volatility compared to the NASDAQ Composite Index, with pronounced peaks and troughs suggesting sensitivity to company-specific and industry events.

Key Risks

The online betting industry is heavily regulated, with laws that vary by jurisdiction. Changes in regulations or increased scrutiny from regulators could affect DraftKings' ability to operate or force changes in its business practices, potentially impacting revenue and profitability.

DraftKings' sports betting business is seasonal, with peak periods during the overlapping NFL and NBA seasons. Off-peak times, such as summer months with fewer major sporting events, can lead to decreased betting activity and revenues.

DraftKings operates in a highly competitive online gambling and sports betting industry. Its current leadership position, shared with FanDuel, faces threats from established players like MGM Resorts International and Caesars Entertainment, as well as new entrants such as Hard Rock Bet and the ESPN betting app by Disney and PENN Entertainment.

Stock Price Target Estimate

Source: Stockpickingsouk

Based on the current market dynamics and the positive tailwinds outlined previously, there appears to be a trend of surpassing the existing estimates. The anticipated price target range of $58 to $60 is viewed with optimism.

Earnings and Sales Revisions by Analysts

The industry tailwinds and Draftking’s capability to take market share are very well reflected in the Earnings and Sales upward revisions by analysts.

Disclaimer

Co-Authors: Michele Filippig, Katerina Kiseleva

Please note that this article represents just one piece of a comprehensive equity research report we prepare on every potential investment idea we consider adding to our portfolio. This content is for informational or educational purposes only and is not to be taken as personalized financial advice. Happy investing!

Remember, all investments carry risk. It's important to practice diligent risk management and conduct your research before making any investment decisions. This content is not intended to provide investment advice.